Accounting for Bank Acquisitions [White Paper]

Key Takeaway

FASB requires that all bank mergers and acquisitions be recorded at fair value. This white paper discusses the accounting requirements for both day one and ongoing accounting.

How Can We Help You?

Founded in 2003, Wilary Winn LLC and its sister company, Wilary Winn Risk Management LLC, provide independent, objective, fee-based advice to over 670 financial institutions located across the country. We provide services for CECL, ALM, Mergers & Acquisitions, Valuation of Loan Servicing and more.

Updated April 2026

Introduction

Banks historically accounted for mergers and acquisitions under the pooling of interest method. The accounting was relatively straightforward and was accomplished by combining the book values of the two entities. Beginning in 2009, the Financial Accounting Standards Board (“FASB”) required bank mergers and acquisitions to be recorded at fair value, making the accounting much more difficult.

Since the purchase accounting rules became effective, we have worked on over 600 merger and acquisition transactions of all sizes, including organizations as small as $2M and as large as over $10B in total assets. We have provided advice on numerous types of transactions including cash/stock deals, mergers of mutual entities, and FDIC-assisted transactions. This white paper is designed to share what we have learned along the way and to address the most common questions we encounter. We hope you find it useful.

We begin with accounting requirements on Day One – the opening journal entries. Next, we discuss the rules for Day Two – the ongoing accounting. Finally, we discuss assessing the goodwill for potential impairment.

Bank Purchase Accounting

FASB ASC 805 Business Combinations requires banks to use purchase accounting and to record the transaction at fair value. As of the acquisition date, an acquirer must record the assets, liabilities and equity of the institution it is acquiring at fair value. The valuation must also include potential intangible assets such as the core deposit intangible. The fair value estimates must be made in accordance with the requirements of FASB ASC 820 Fair Value Measurements and Disclosures. Please refer to Appendix A for a comparison of the “old” rules to the “new” rules.

Wilary Winn notes that the business combination accounting rules can apply to a transaction that is not a full acquisition, including branch acquisitions, purchase and assumption agreements, etc.

Determining whether a financial institution has acquired a business or has consummated an asset purchase is a critical first step because:

- Goodwill is recognized in a business combination, but not in an asset acquisition;

- Acquisition costs are generally expensed as incurred by the buyer in a business combination, while the same costs are considered part of the acquisition cost in an asset acquisition; and

- Assets acquired and liabilities assumed in a business combination are measured at fair value, while assets acquired and liabilities assumed in an asset acquisition are measured by allocating the total cost of the net assets based on the fair values of the individual assets acquired and liabilities assumed.

Day One Accounting

The first step a bank should take upon acquiring the assets of another financial institution is to determine whether it has acquired a business. We note that under FAS ASC 805, a business combination occurs when a buyer obtains control of a business through a transaction or other event. A “business” includes inputs and processes that are at least capable of producing outputs. However, a business need not include all of the inputs or processes that the seller used in operating the business if market participants are capable of acquiring the business and continuing to produce outputs, for example, by integrating the business with their own inputs and processes1.

When a financial institution enters into a transaction to combine with another entire institution, the result is clearly a business combination. Wilary Winn believes that the acquisition of a bank branch also meets the definition of a business combination because the branch has inputs, processes, and can produce outputs. On the other hand, an acquisition of a loan portfolio would not meet the definition of a business. Determining whether sufficient inputs and processes have been acquired can require considerable judgment and we encourage acquirers to discuss the accounting implications of an acquisition with their external accountants and primary regulators.

Once it has determined that it has entered into a business combination, the acquiring bank must undertake several steps to ensure it has the information it needs to properly record the transaction.

It must determine the:

- Fair value of the consideration transferred;

- Fair value of the acquired bank’s financial assets and liabilities;

- Fair value of the acquired banks non-financial assets and liabilities;

- Fair value of any intangible assets – the most common being the core deposit intangible;

- Fair value of the trade name; and

- Amount of goodwill/bargain purchase gain resulting from the transaction.

Fair Value of the Consideration Transferred

Valuation experts generally use differing methods to determine fair value. Wilary Winn employs three basic methods to determine the fair value of the consideration provided to the seller: discounted cash flow (“DCF”), guideline transaction (“GT”), and guideline public company (“GPC”). The DCF method is an income approach, whereas the GT and GPC methods are market approaches.

Discounted Cash Flow Method

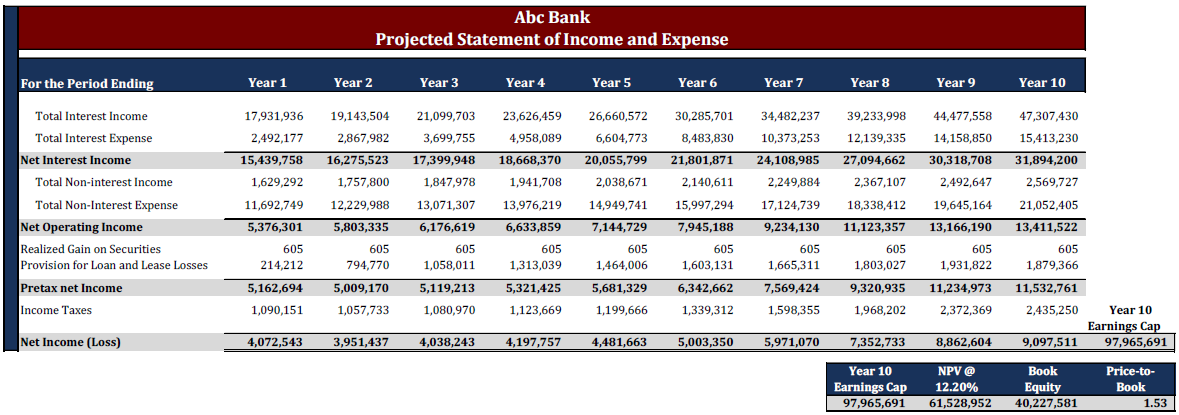

The DCF method determines the value of a business or business ownership interest using one or more methods that convert anticipated benefits into a present single amount. The application of the DCF method establishes value by methods that discount or capitalize earnings and/or cash flow, by a discount or capitalization rate that reflects market rate of return expectations, market conditions, and the relative risk of the investment. To determine the estimated value of the entity using a DCF approach, business appraisers generally first estimate the organization’s probable future cash flows. They then discount the cash flows back to the valuation date at an appropriate discount rate. However, Wilary Winn believes that the use of future cash flows is not a reliable indicator of value for financial institutions because items like capital expenditures, working capital, and debt are not clearly defined. As a result, to ensure comparability, we base our analysis on future earnings.

To determine the estimated value of the entity using a DCF method, Wilary Winn estimates future earnings by developing ten-year pro-forma balance sheets and income statements using a fundamental analysis. We then develop an estimate for the entity’s lifetime earnings – “the residual” using a Gordon growth model. We discount the resulting estimated cash flows back to the valuation date at a discount rate determined through use of a Capital Asset Pricing Model (“CAPM”) approach. See below for an example.

Market Approaches

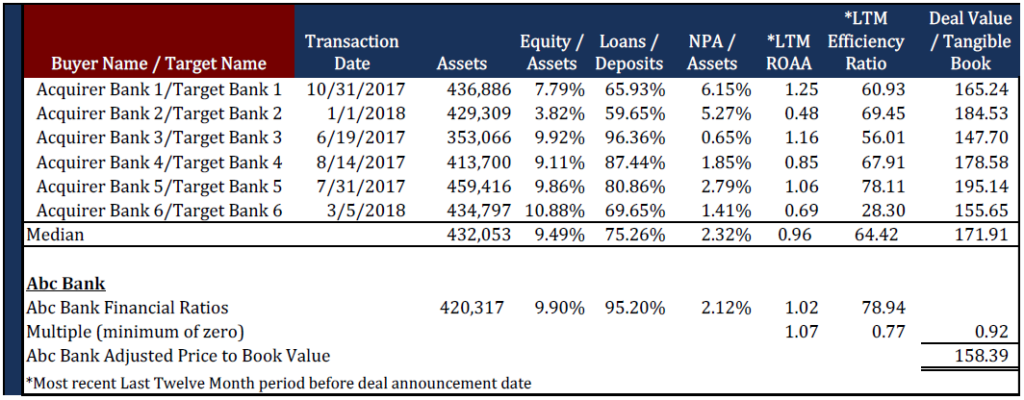

In addition to the DCF method, we utilize two market approaches – Guideline Transaction (“GT”) and Guideline Public Company (“GPC”). Under the GT method, we obtain deal results and financial information for recent bank acquisitions of similar size, similar profitability, and in similar geographic areas to banks we are valuing. To obtain our estimate of value, we use the median price to tangible book value from our pool of deal results. An example of our GT method is shown below.

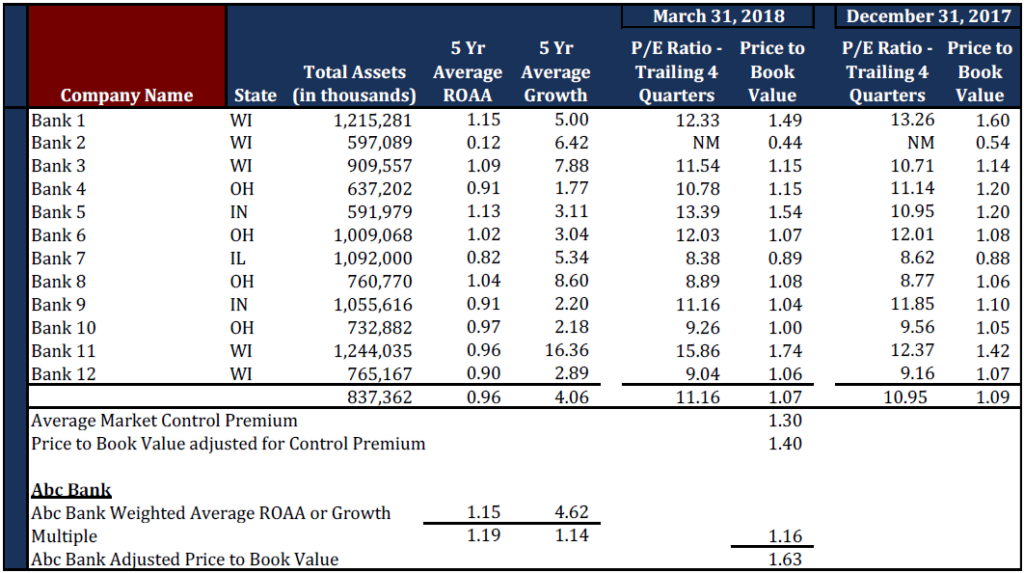

Under the GPC method, we obtain recent financial information on publicly traded community banks of similar size, similar profitability, and in similar geographic areas to the banks we are valuing. To obtain our estimate of value, we use the median price to tangible book value from our pool of community banks. We then adjust for the premium a market participant would pay for majority control of the entity. An example of our GPC method is shown below.

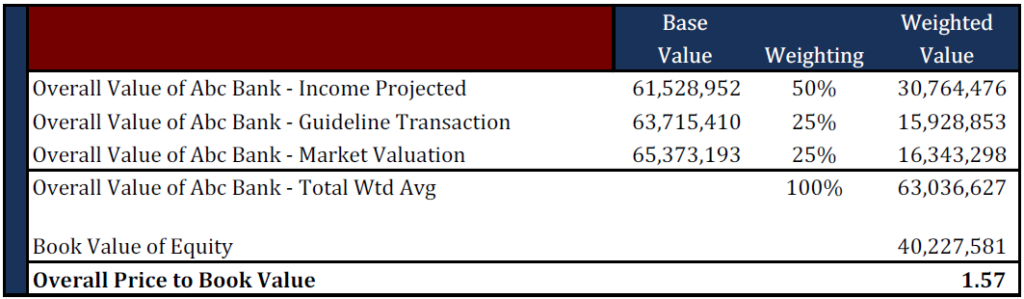

Finally, we reconcile the valuation estimates derived under the three methods and determine the overall fair value of the acquired bank. We note that we weight the DCF method the highest, as we believe this method is most representative of the bank’s current financial position and potential future earnings.

Our overall valuation results serve as a market comparison when the acquirer is paying cash. However, when a bank is acquiring another financial institution using its own stock, the valuation approaches are integral to properly accounting for the transaction.

Fair Value of Financial Assets and Liabilities

The financial assets and liabilities consist primarily of loans, investments, deposits, and debt. Accrued interest receivable, accounts receivable, accrued interest payable and accounts payable are also considered to be financial assets or liabilities.

Investments

Investments generally consist of certificates of deposits (“CDs”) and “vanilla” bonds. To determine the value of a CD, Wilary Winn discounts the expected cash flows using an estimated market interest rate over its expected remaining life. We can generally identify a price for the bonds using Bloomberg or another pricing service. We occasionally encounter illiquid securities, which we value using a discounted cash flows approach.

Wilary Winn notes there are benefits to having the acquiring institution’s bond accounting service value the investments. In this instance, we perform a reasonability check to ensure the investments are appropriately priced.

Accounts Receivable and Payable

Wilary Winn generally values the short-term accruals, accounts receivable and accounts payable at book value, because we believe the present value effect is immaterial.

Deposits

The fair value of the deposit accounts is dependent on whether they are time or non-time deposits. The non-time deposits are recorded at book value. The value of the non-time deposits is reflected in the “core deposit intangible.” The valuation of intangible assets is discussed in the Intangible Assets section later in this paper.

Wilary Winn estimates the value of time deposits in a manner similar to the one we use for certificate of deposit investments.

Debt

Wilary Winn generally values two differing types of bank debt: Federal Home Loan Bank (“FHLB”) advances and subordinated debt. We use a discounted cash flow approach to value any outstanding debt.

Loans

Wilary Winn believes that determining the fair value of the loans is one of the most complex undertakings under the purchase accounting rules. The marketplace for seasoned loans is not active. As a result, valuation experts generally value the loans using a discounted cash flow analysis. Two approaches are permissible under GAAP2. One approach is to discount the contractual cash flows at an “all in” estimated market discount rate, which by its nature includes a credit spread. The other approach is to develop a “best estimate of expected cash flows” and discount the amounts back to the valuation date at an appropriate discount rate. We employ the second method.

We estimate the fair value of the loan portfolio by performing a discounted cash flow analysis using a proprietary valuation model. The valuation is performed at the loan level on real estate and commercial loans and at the cohort level for all other loan types, and is based on the objective attributes of the loans in the portfolio (e.g., the rate of interest on the loan, the original term of the loan, the current term of the loan, etc.) and current statistical performance variables used in the marketplace. Our analysis is based on the contractually specified amounts of principal and interest to be received, modified by our estimates of prepayment, default and loss severity to be experienced prospectively. Our prepayment, default and loss severity assumptions are applied at the loan or cohort level based on the characteristics of the loan (type of loan – CRE vs. C&I, risk ranking – pass vs. substandard, etc.).

We derive our expected prepayments using a conditional repayment rate (CRR), which is the annual amount of expected voluntary payoffs as a percentage of the principal amount outstanding at the beginning of the year. We model our defaults using a conditional default rate (CDR), which is the annual amount of expected defaults as a percentage of the principal amount outstanding at the beginning of the year. Finally, our loss severity is equal to the liquidated principal balance minus any recovered amount divided by the principal balance. The combination of the CDR and loss severity derives our future lifetime loss assumptions.

For larger loans such as those collateralized by commercial real estate, we rely on our client’s estimates of expected credit losses or reserve percentages – especially loans with lower credit quality. In our experience, banks typically review these loans in detail as part of their credit risk management, and we rely on loss estimates from such reviews for our estimates.

We develop a “best estimate of expected cash flows” for all loans and use a buildup method to develop our discount rate. We begin with an appropriate risk-free rate based on the term of the loan (adjusted for amortization, voluntary, and involuntary prepayments), and add a spread for uncertainty, liquidity, and increased costs to service for loans with lower FICO scores, high-risk rankings (watch list, substandard, etc.), or delinquent loans. Because we are using expected cash flows net of credit losses, our discount rates for loans do not include a credit spread. Wilary Winn believes including the credit spread in the discount rate would be “double counting.”

The book value of the loans is thus adjusted for an interest rate differential (discount rate adjustment) and an estimate of expected credit losses (credit loss discount).

Due to the estimated fair value of the loans, including the estimated credit losses, the allowance for credit losses is recorded at zero on day one.

See the adjustments to loans in the example loan summary attached as Appendix C – the interest rate discount – $1,586,077 in total and the credit loss discounts – $826,981 in total. See the Day Two accounting section of this white paper for more details.

Prepaid Expenses

The treatment of prepaid expenses can be complex. One should consider whether the prepaid item would have benefit to market participants. For example, a multi-year prepaid contract that cannot be used after the acquisition would have no “fair value” and would be recorded at zero in the Day One journal entry.

Accrued Liabilities

Wilary Winn recognizes that prior to the change in the accounting rules, many acquiring organizations had the acquired bank accrue the costs of the acquisition on its financial statements prior to the acquisition so the expenses would not flow through the income statement of the combined entity. This is another significant change to the rules.

In general, the costs of the acquisition and any restructuring costs should flow through the income statement of the acquiring bank3.

The theory is that if the party that receives the primary benefit is the acquirer or the combined entity, the cost should run through its income statement. In our experience, the types of costs that can be accrued as part of the acquisition are quite limited. An example would be a compensation arrangement that was in place before the acquisition was contemplated, and that just happens to be triggered as a result of the acquisition. The required payout can be accrued on the acquired bank’s financial statements as of the acquisition date. By way of contrast, a payout negotiated as part of the acquisition should run through the income statement of the acquiring bank.

The acquiring bank should also ensure that the acquired bank has properly accrued its expenses. In other words, the organization should ensure that the acquired bank does not have any unrecorded liabilities.

Fair Value of Non-Financial Assets and Liabilities

The most significant non-financial assets are generally land and buildings. We generally require our clients to obtain commercial real estate appraisals if these assets are material.

Real estate leases are another item that must be evaluated in an acquisition. If the lease price is less than the market rate, then an asset should be recorded. On the other hand, if the lease price is over the market rate, a liability should be recorded. We calculate these items by discounting the difference in cash flows back over the remainder of the lease term to the valuation date at the acquired bank’s estimated cost of capital.

Intangible Assets

The value of intangible assets should be recorded as well in the Day One journal entry.

Recognition of an intangible asset requires that the asset be separable or have a contractual or legal benefit.

The most common intangible assets in a bank acquisition are:

- Mortgage servicing rights

- Core deposit intangible

- Customer relationships

- Value of the acquired bank’s trade name

- Goodwill

Mortgage Servicing Rights

Mortgage servicing rights are the rights to service a loan that has been sold into the secondary market in exchange for a fee. The market for bulk sales of mortgage servicing rights is quite limited. As a result, the value of mortgage servicing rights is generally determined via a discounted cash flow analysis. The most sensitive input in the valuation is the assumption regarding the rate at which the loans will prepay.

Core Deposit Intangible

The premise underlying the core deposit intangible asset is that a rational buyer would be willing to pay a premium to obtain a group of core deposit accounts that are less expensive than the buyer’s marginal cost of funds. Wilary Winn believes the core deposit intangible benefit depends on the type of account. For example, share draft accounts have very different economics and behavior than high-rate money market shares. To calculate the estimated fair value of the core deposit intangible, we first segment the accounts by type. Next, we estimate the likely decay, average life, and terminal economic life. The rate paid on the deposit, the non- interest income generated, and the non-interest expense incurred also affect the value of the core deposit intangible. Wilary Winn estimates the value of the core deposit intangible through a discounted cash flow analysis.

Customer Relationships

Wilary Winn believes that the value of the customer relationships is imbedded in the purchase price of the institution. We believe it would be quite difficult to separately determine the value of customer relationships in terms of the ability to cross-sell loans or deposits at lower cost, or higher rates of penetration, and therefore, have generally not seen such items recorded.

Acquired Bank’s Trade Name

A trade name can have value based on how widely it is recognized. If the brand is well known and the acquiring bank intends to continue to utilize it, the trade name has value. Trade names can also have a defensive value. That is, it can have value even though the acquiring bank plans to retire the name. For example, imagine the value to Pepsi of having the rights to the Coca-Cola brand name.

Goodwill Or Bargain Purchase

On Day One, the acquiring bank records the fair value of the assets acquired and liabilities assumed and the fair value of any intangible assets.

The amount required to balance the Day One journal entry is Goodwill or a Bargain Purchase. Wilary Winn believes an acquisition will generally result in goodwill, as opposed to a bargain purchase gain.

In fact, GAAP requires the acquiring bank to “double check” its work before recording a bargain purchase4.

If the acquiring bank is privately held, it can elect to account for the resulting goodwill in one of two ways. The bank can amortize the goodwill straight-line over a period not to exceed 10 years. Otherwise, it can elect not to amortize the goodwill and instead assess it for impairment. The assessment must be made at least annually. Publicly traded banks must use the impairment assessment method.

In our experience with acquisitions involving bank holding companies, we typically see the acquired goodwill recorded at the level of the transaction. For example, if the bank holding companies merge and the consideration transferred is at the bank holding company level, we would generally see the goodwill recorded on the bank holding company’s balance sheet. However, we note that entities can elect to apply pushdown accounting to its reporting entities subsequent to the acquisition in accordance with FASB ASC 805-50-15-10.

Income Taxes

The discussion regarding income taxes which follows is a brief summary of information contained in RSM’s “A Guide to Business Combinations – Third Edition June 2016.” We thank them for allowing us to reference it in this white paper and encourage those who want more detail to consult the RSM guide or contact your tax practitioner.

For income tax purposes, business combinations are considered taxable or nontaxable. Asset acquisitions are taxable to seller. Nontaxable transactions take two forms. A transaction could be nontaxable because the financial institution is an S Corporation or, in the case of C Corporation, the buyer purchases stock – a “stock acquisition.” A stock acquisition can be turned into a taxable event if the buyer and seller elect to treat it as such under Section 338 of the U.S. Income Tax Code – a “338 Election.”

The required accounting for income taxes in a business combination is set forth in FASB ASC 805-740, which differs from the fair value determinations we have discussed thus far. The first difference is that deferred tax assets and liabilities are measured on an undiscounted basis. In addition, to be recognized, the deferred tax asset must be more than 50 percent likely of being realized.

Taxable transactions will have few temporary differences between book and tax as the basis for most assets and liabilities will be the same. Nontaxable transactions often result in several temporary differences. The tax bases of the assets and liabilities of the target will be the same post-acquisition as they were prior to the acquisition (carryover basis), while the book values will be based on fair value.

See Appendix B1 & B2 for an example comparing the fair value of the balance sheets of a subsidiary bank and the bank holding company to the book values at the acquisition date. Additionally, the goodwill and bargain purchase calculation is included on these appendices. Appendix D shows how to record the acquisition on Day One, including the accounts used to adjust book value to fair value at the bank and bank holding company level.

Wilary Winn further notes that GAAP allows the acquiring bank to true up the Day One journal entry for up to 12 months after the acquisition date to reflect new information that would have affected the valuation amounts had they been known5.

We note that the “new” information is relative to the acquisition date only. The adjustment is designed to reflect information that existed as of the valuation date that was not known at the time. It is not intended to reflect changes in facts and circumstances as of the valuation date. Instead, it is designed to reflect a clarification of facts that existed as of the valuation date. For example, if a loan at the valuation date was a modified loan and was not disclosed as such, an adjustment would be appropriate. On the other hand, if the acquired bank obtained an appraisal for a branch location at the acquisition and due to changes in market conditions, the value of the branch was less 11 months later, an adjustment would not be appropriate.

Day Two Accounting

Many find the day one accounting to be relatively complex. The ongoing accounting for the recorded premiums and discounts is also quite complex. The following is a quick summary for the items other than loans, followed by a detailed description of the required ongoing accounting for the acquired loans.

The premiums or discounts for the investments acquired are amortized or accreted into income over the estimated life of the investment as an adjustment to interest income. Premiums reduce interest income, whereas discounts have the opposite effect.

The premiums or discounts on the acquired debt and time deposits are amortized or accreted into expense over the estimated life of the liability as an adjustment to interest expense. Premiums reduce interest expense, whereas discounts increase interest expense.

Mortgage servicing rights acquired in the acquisition are generally amortized on a level-yield basis over the estimated life of the loans. The amortization is recorded as a reduction to servicing income. We note that mortgage servicing rights can also be measured and reported on an ongoing basis at fair value, with the change in fair value running through the income statement. This fair value accounting is generally used by large institutions, which have generally hedged the portfolio against interest rate risk.

The core deposit intangible is amortized on a level-yield over the estimated lives of the non-time deposits. The expense should be recorded as a reduction to non-interest income.

The fair value of the fixed assets acquired becomes the basis for depreciation. The fixed assets should be depreciated over their estimated remaining lives, which can be longer or shorter than the term used to calculate depreciation before the acquisition.

The most complex ongoing accounting relates to the acquired loans.

Non-PCD Assets and Purchased Financial Assets with Credit Deterioration

The Current Expected Credit Losses (“CECL”) standard (FASB ASC 326) requires the acquirer in a business combination to estimate lifetime expected credit losses on all acquired financial assets. Historically, this created two separate accounting frameworks, purchased credit deteriorated (“PCD”) and non-PCD, each with different implications for the day one measurement of acquired loans, as described below.

PCD Assets: These assets have experienced “more-than-insignificant” deterioration in credit quality since origination based on an assessment by the acquirer as of the acquisition date. Under the PCD model, the acquirer records an allowance for credit losses (“ACL”) related to the PCD assets and also records an offsetting entry as an addition to the purchase price of these assets. In other words, the initial amortized cost basis that would be recorded for PCD assets is equal to the sum of the purchase price and the ACL. This method is typically referred to as the gross-up approach. Furthermore, any remaining purchase discount or premium that is not credit-related is accreted or amortized to interest income over the life of the assets.

Non-PCD Assets: These acquired assets do not meet the PCD criteria and are accounted for in a manner consistent with originated financial assets. Specifically, the acquirer must provision for these assets on Day 1 as a charge to credit loss expense. Additionally, the institution would record the amortized cost basis of these assets at the purchase price paid for them. Thereafter, any purchase discount or premium is accreted or amortized to interest income over the life of the assets. As a result of the Day 1 charge to credit loss expense and lack of a step-up in basis for expected credit losses, many industry participants describe this accounting as the “Day 1 double count.”

Please see an example below highlighting the difference in day one impact between PCD and non-PCD assets.

Stakeholders expressed that the dual approach is operationally complex, inconsistent, and unintuitive. Investors, preparers, and other stakeholders have advocated for a uniform treatment of all acquired financial assets. In particular, they indicated that they preferred the gross-up approach applied to non-PCD assets, citing improved comparability, reduced complexity, and alignment with economic substance.

On November 12, 2025, the FASB issued ASU 2025-08, delivering long-awaited reform to the CECL standard. This update establishes a single accounting model for acquired loans. Under the updated guidance, all loans acquired in a business combination, except for credit cards, are classified as purchased seasoned loans (“PSLs”) and accounted for using the gross-up approach previously applied only to PCD loans. Accordingly, the initial amortized cost basis of PSLs equals the purchase price plus the initial ACL recorded at acquisition. The non-credit discount or premium is subsequently accreted or amortized to interest income over the expected life of the loans.

Purchased Seasoned Loans

Key provisions relating to FASB’s recent update are highlighted below.

Objective: The FASB retained the current accounting for PCD assets but revised the ASU to improve the accounting for non-PCD assets that did not fall under the PCD scope. As a result, the current PCD accounting model is unchanged.

Scope: All acquired loans except for credit cards will be classified as PSLs and be subject to PCD framework.

Seasoning: All loans, except for credit cards, would be considered seasoned and fall under the scope of the new standard if they are acquired through a business combination. In an instance where a pool of loans is purchased via an asset acquisition, the acquirer must then perform a seasoning test to determine whether the acquired loans would qualify to be accounted for under the gross-up approach. This seasoning test classifies loans purchased 90+ days after origination and where the buyer was not involved in the origination as PSLs.

Disclosure, Transition, and Effective Date: The ASU’s guidance is effective for annual reporting periods beginning after December 15, 2026, including interim reporting periods, and entities must apply it prospectively. Entities may early adopt the guidance “in an interim or annual reporting period in which financial statements have not yet been issued or made available for issuance.” An entity that adopts the amendments in an interim reporting period may apply them “as of the beginning of that interim reporting period or the beginning of the annual reporting period that includes that interim reporting period.”

In summary, the specifics for PSLs are as follows:

- At acquisition, a financial institution will estimate and record an allowance for credit loss, which is then added to the purchase price.

- Favorable and unfavorable changes in expected credit-related cash flows will run through the allowance and credit loss expense.

- Non-credit premium or discount will be accounted for based on the effective yield after the gross-up for the allowance.

Purchased Seasoned Loans – Example

The example shown below illustrates the accounting for PSLs under CECL. The financial institution purchased a loan with a principal balance of $100,000 for $77,500. It set the initial reserve for expected credit losses at $15,000. It also recorded a purchase discount of $7,500, which it will amortize on a level-yield basis.

The contractual P&I payment is $1,887 per month. The stated interest rate on the loan is 5%.

At the end of month two, the financial institution reevaluates the loan and determines that the loan is riskier than it thought. It records a $5,000 increase in the credit reserve based on its new estimate of the amount of principal it will receive.

In month three, it agrees to extend the maturity date of the loan because it believes the extension will aid the borrower and will result in the receipt of $11,500 in additional principal over the life of the loan. Therefore, it reduces the credit reserve by $11,500. The contractual P&I is modified to $1,045 per month. In addition, it lowers the amount of discount accreted from $251 to $128, reflecting the lengthening of the maturity date from 5 years to 10 years.

In month 4, the borrower informs the financial institution that it has a firm offer on the property and intends to repay the loan with the proceeds in full. The financial institution believes there no longer is a credit risk on the loan and relieves the remaining ACL amount of $8,500 to provision expense.

In month 5, the borrower repays the loan in full. The remaining discount is released into income.

The monthly journal entries are shown below along with a table summarizing the results.

The ASU directly addresses one of the industry’s most significant CECL pain points: non-PCD loans required a Day 1 provision despite the fair value determination already reflecting expected losses. The result was an unintuitive double count of the credit mark. By expanding gross-up accounting to PSLs, ASU 2025-08 represents a significant improvement to purchase loan accounting since the CECL standard’s introduction, as it simplifies purchase accounting, improves comparability, and better reflects economic reality.

Finally, we note that examples of templates used to amortize/accrete the fair value adjustments for all the accounts, including the loan adjustments, are attached as Appendix E.

Accounting for Goodwill

If the acquiring bank is privately held, it can elect to account for the resulting goodwill in one of two ways. The bank can amortize the goodwill straight-line over a period not to exceed 10 years.

Wilary Winn cautions that in order to use this method, the bank must make an irrevocable accounting election. The election affects the existing goodwill, as well as any additional goodwill acquired in the future6.

Otherwise, it can elect not to amortize the goodwill and instead assess it for impairment. The assessment must be made at least annually. Publicly traded banks must use the impairment assessment method.

The process begins by determining the entity to be assessed. In our experience with acquisitions involving bank holding companies, we typically see the acquired goodwill recorded at the level of the transaction. For example, if the bank holding companies merge and the consideration transferred is at the bank holding company level, we would generally see the goodwill recorded on the bank holding company’s balance sheet. However, we note that entities can elect to apply pushdown accounting to its reporting entities subsequent to the acquisition in accordance with FASB ASC 805-50-15-10.

Perhaps counter-intuitively, the goodwill test is nearly always performed at the combined entity level instead of at the level of the acquired bank. The test would be performed at the acquired bank level only if it were deemed to be a separate operating segment or a component of a separate operating segment. An entity must have all the following characteristics to be deemed a separate operating segment7:

- It engages in business activities from which it may earn revenue and incur expenses;

- Its discrete financial information is available; and

- Its operating results are regularly reviewed by the chief operating decision maker (“CODM”) to make decisions about resources to be allocated to the segment and assess its performance.

Wilary Winn believes most acquired banks would not be considered a separate operating segment. However, one example would be if a bank holding company acquired a bank, pushed the goodwill down to the bank, and did not merge the bank with its other subsidiary banks. In this case, the target bank, not the combined bank holding company, would be the reporting unit for goodwill impairment testing.

The assessment for goodwill impairment can be qualitative or quantitative.

Qualitative Testing

A bank may assess qualitative factors to determine whether it is more likely than not (that is, a likelihood of more than 50 percent) that the fair value of the reporting unit is less than its carrying amount, including goodwill. In evaluating whether to perform the qualitative test, the guidance requires an entity to assess relevant events and circumstances. Examples of such events and circumstances include the following8:

- Macroeconomic conditions, such as deterioration in general economic conditions, limitations on accessing capital, fluctuations in foreign exchange rates, or other developments in equity and credit markets.

- Industry and market considerations, such as a deterioration in the environment in which an entity operates, an increased competitive environment, a decline (both absolute and relative to its peers) in market-dependent multiples or metrics, a change in the market for an entity’s products or services, or a regulatory or political development.

- Cost factors, such as increases in raw materials, labor, or other costs, that have a negative effect on earnings.

- Overall financial performance, such as negative or declining cash flows or a decline in actual or planned revenue or earnings.

- Other relevant entity-specific events, such as changes in management, key personnel, strategy, or customers; contemplation of bankruptcy; or litigation.

- Events affecting a reporting unit, such as a change in the carrying amount of its net assets, a more-likely-than-not expectation of selling or disposing all, or a portion of, a reporting unit, the testing for recoverability of a significant asset group within a reporting unit, or recognition of a goodwill impairment loss in the financial statements of a subsidiary that is a component of a reporting unit.

Quantitative Testing

If, after assessing the totality of events or circumstances described in the paragraphs above, a bank determines that it is more likely than not that the fair value of a reporting unit is less than its carrying amount, then the bank must perform a quantitative goodwill impairment test.

The quantitative test (previously called “Step One”) determines whether the fair value of the combined entity exceeds its book value using the income and market approaches described at the beginning of this white paper. If the fair value of the combined entity exceeds the book value, the goodwill is not impaired9. If the fair value of the combined entity does not exceed book value, entities will record an impairment charge based on the excess of a reporting unit’s carrying amount over its fair value.

Wilary Winn notes that the FASB issued guidance in January 2017 that eliminates the requirement to calculate the implied fair value of goodwill (e.g., Step Two of the previous goodwill impairment test) to measure a goodwill impairment charge. Entities will rather record an impairment charge based on the excess of a reporting unit’s carrying amount over its fair value (e.g., based on today’s Step One). The revised standard did not change the guidance on completing Step One of the goodwill impairment test. Additionally, an entity can still perform the current qualitative goodwill impairment test prior to determining whether to proceed to Step One.

Conclusion

While the initial and ongoing required accounting can be complex, Wilary Winn does not believe that the rules should deter transactions that otherwise make sense. We have worked with our clients, their external auditors, and the regulators to ensure our clients have the information and knowledge they need to successfully undertake these transactions. We hope you have found this white paper to be informative and useful.

Please download the PDF at the top of this page to view all appendices